Well I spent the holiday weekend with in-laws in Louisville, KY. My mother in-law gets about 32 channels, so I was flipping on Sunday morning. I wish I hadn't. Fourteen of the 32 channels were church broadcasts. I guess if you have an extra thousand bucks a month or whatever, you can broadcast yourself.

Newsflash: just because you can do something doesn't mean you should. I'm not sure that I've heard such fear-mongering and hate-baiting in all my life. It made me sick and embarrassed to be a Christian. Is it any wonder the world thinks so poorly of us, when junk like this is pumped through the airwaves at us?

I think at least 8 of the 14 stations were preaching on the end times and how bad it's going to be for people left behind. Good grief, people. Don't we have bigger fish to fry? Isn't there some good news in here some place? Christmas weekend, no less. People flipping through with their families, full of holiday cheer and they get this message? Not only the message, but detailed maps on where the horror is going to take place and what nationalities are going to get filleted like fish.

It honestly makes me want to puke. Our loudest dogs keep doing all the barking for the rest of us. They're like that yappy neighbor dog that won't shut up in the morning. You know the one... he has no idea what he's barking at or what he's barking for. He's just barking because he can. I think it's past time for Christians to stand up and tell this people to take the three-ring circus someplace else.

Tuesday, December 30, 2008

Monday, December 22, 2008

The Happening, M. Night Shyamalan

Whenever critics get particularly miffed about a movie, I tend to make myself watch it. We're a couple of days off from Christmas, what better time than now to watch M. Night Shyamalan push from his self-described PG-13 mindset to a rated R? Tis' the season for mindless violence, right?

Sigh. I was slightly disappointed, but certainly not enough to go trouncing over the guy's creativity, as did some critics. Maybe he just wanted to see what he could do with a R rating... a pushing of the envelope so to speak.

I want to go on record as stating the film would have worked better as a PG-13. The violence was distracting by what was otherwise an above average script. The premise was standard Hollywood blather: we're killing the earth and there by killing ourselves. Shyamalan takes it to a literal extreme that I think would have been much more effective if passed off as an under-current, tugging gently at our ankles while we lounge in knee-deep salt water.

Instead, he gives us a tidal wave and thereby leaves us shrugging our shoulders at the end. I pretty much ejected the DVD thinking, "Nice story man, but now it's time to put that crap out of my head." The themes themselves were nothing short of masterful. He just used a sledge-hammer when a chisel would have gotten more mileage.

But that's not why I'm bothering to blog it. I'll watch anything the man puts out because I believe he is brilliant. No, I'm blogging tonight for what the medium of film always does-- it tells us about ourselves. With The Happening and the newly released Seven Pounds, it would appear that we're on a suicide motif this year.

2008 -- the year we killed ourselves. I don't believe that vaguely similar themes appearing in blockbuster films are coincidence so much as I believe that C.G. Jung had a mind second only to that of Shakespeare. Our subconscious will find a way to express itself, one way or the other.

Both of these films take us to what we dare not speak outloud. Culturally, we're priming the pump to carry out a hidden death wish. I'd take the thought further, but it's late and I'm tired. Just saying, it matters. That's all.

Sigh. I was slightly disappointed, but certainly not enough to go trouncing over the guy's creativity, as did some critics. Maybe he just wanted to see what he could do with a R rating... a pushing of the envelope so to speak.

I want to go on record as stating the film would have worked better as a PG-13. The violence was distracting by what was otherwise an above average script. The premise was standard Hollywood blather: we're killing the earth and there by killing ourselves. Shyamalan takes it to a literal extreme that I think would have been much more effective if passed off as an under-current, tugging gently at our ankles while we lounge in knee-deep salt water.

Instead, he gives us a tidal wave and thereby leaves us shrugging our shoulders at the end. I pretty much ejected the DVD thinking, "Nice story man, but now it's time to put that crap out of my head." The themes themselves were nothing short of masterful. He just used a sledge-hammer when a chisel would have gotten more mileage.

But that's not why I'm bothering to blog it. I'll watch anything the man puts out because I believe he is brilliant. No, I'm blogging tonight for what the medium of film always does-- it tells us about ourselves. With The Happening and the newly released Seven Pounds, it would appear that we're on a suicide motif this year.

2008 -- the year we killed ourselves. I don't believe that vaguely similar themes appearing in blockbuster films are coincidence so much as I believe that C.G. Jung had a mind second only to that of Shakespeare. Our subconscious will find a way to express itself, one way or the other.

Both of these films take us to what we dare not speak outloud. Culturally, we're priming the pump to carry out a hidden death wish. I'd take the thought further, but it's late and I'm tired. Just saying, it matters. That's all.

Tuesday, November 25, 2008

Give me a $1 and I will make it easy for you to borrow it back!

CNN has the full details but it hardly matters, I suppose. Nothing has mattered to this point... the 700 Billion Dollar bailout plan is now it's fourth incarnation. This time, Paulson has set his sites on consumer lending. The theory is real simple-- make it easier for Americans to borrow money on their cars, colleges, and credit cards. When it's easy to borrow, it's easier to spend. The hope is to jump start the GDP which just saw it's biggest quarterly decline in 27 years. Americans just don't have any more money to spend, disposable income is down, debt is up. So what do you do when disposable income is down? Make it easier to borrow. Funny how it never occurred to Paulson that maybe putting more money in the hands of consumers would be better than putting more debt in their laps. Nah, that's be too simplistic. The answer -- take money away from consumers with taxes. Then offer to give them more debt in exchange for it. That makes good sense, doesn't it. I mean if I offered to take $1 from you, then promised to make it very easy to borrow that dollar right back from me-- you'd go for it wouldn't you? Awww, come on. It's me!

Stupid is as stupid does, and Paulson must be jockeying for an award. Taking money from our children and our children's children to fund our drunk-lust spending spree as Americans is just plain stupid. Not only are we left with the taxation credit card bill (which we owe to China no less), we're also making sure that the plastic can keep flowing, both through the credit card machines and that the National Shopping Bag Workers Union stays in business.

So, buckle up folks. Just in time for the holidays, Secretary Paulson has unleashed a new plan to stimulate consumer borrowing. Get in line early, folks because your friendly neighborhood slavers have never offered prices this low!!!

Thursday, November 20, 2008

The Slaver Bailout Plan of 2008

So the Dow hit a record low for the decade just a few moments ago, taking us back to numbers which haven't been seen since the Clinton era. Personally, I think we are near the bottom, but jeez... who can really tell?

Of course, this crash is happening in the middle of the largest bailout of corrupt businesses and corporate greed in the history of the United States. Having already spent almost half that 700 billion in two months, Americans still haven't seen anything. Jobs are not being created; they are being lost. Credit isn't being freed up, or at least if it is, very few are getting sucked in. Rates are the lowest they've ever been, but Americans are too in debt to take on more debt.

Once again, wisdom is proved by all her children. The solution to America's credit crisis was never more credit, cheaper credit, and easier to attain credit. You don't fix credit with credit. Ask anyone who is busy rolling around card debt from lender to lender to squeeze out an extra $20 bucks per month. It's a miserable place to be, I know from experience.

Tennessee is suffering. Because we don't have an income tax, we depend on sales tax revenue. Other states are hurting too because much of their budget is based on sales tax revenue. But what can you do when there are no sales? Free up credit? Further strangle our nation in a choke-hold of debt? Print more money?

Your government's solution was to bail out the slavers, not the slaves. To reward corruption and greed with billions of your children's tax dollars, ensuring that your children will also be slaves. Since passing the slaver bailout plan, the United States government has experimented with three different ways to spend it. None of that has your best interest in mind because it doesn't add a penny to your pocket; it just makes it easier for you borrow a penny from theirs.

Once again, all this money that is going to banks to erase invisible debt would have been better placed in the hands of working Americans with real debt. They sold invisible money; Americans acquired real debt. The slavers got caught with their hands in the cookie jar.

We are running out of both time and choices. If you subtract the illegal immigrants and the population of Americans under the age of 18, then remove all non-working and un-taxable Americans, you'd be left with well under 200 million people. Divide out that 700 billion dollars (which by the way is ours) and you'd have a stimulus package totaling around $13,000 for my family of two working adults. That's a bailout ladies and gentlemen!

$13,000 of additional income to liquidate debt, to pump into the economy, to boost the Tennessee sales tax revenue, to invest in the markets.... the possibilities are endless. The government could have put requirements on the money-- forcing all working Americans with debt to put their full stimulus package toward their debt. And non-working Americans and illegals? Well they should have never been given credit to begin with. Let the slavers suffer. This action would have created liquidity-- and given real capital for the slavers who were responsible in their lending as their working slaves climbed out from under their clutches toward financial freedom.

Instead they chose to keep us slaves. And the ones that hurt the most? Working Americans. It's time for action, people. Are GM and Ford going to fail whether we bail them out or not because they have demonstrated the failure to make wise choices. We don't have to go softly into that goodnight. Write your congressman. Tell them they've rewarded quite enough stupidity, ignorance, and greed for this lifetime, and the next.

Of course, this crash is happening in the middle of the largest bailout of corrupt businesses and corporate greed in the history of the United States. Having already spent almost half that 700 billion in two months, Americans still haven't seen anything. Jobs are not being created; they are being lost. Credit isn't being freed up, or at least if it is, very few are getting sucked in. Rates are the lowest they've ever been, but Americans are too in debt to take on more debt.

Once again, wisdom is proved by all her children. The solution to America's credit crisis was never more credit, cheaper credit, and easier to attain credit. You don't fix credit with credit. Ask anyone who is busy rolling around card debt from lender to lender to squeeze out an extra $20 bucks per month. It's a miserable place to be, I know from experience.

Tennessee is suffering. Because we don't have an income tax, we depend on sales tax revenue. Other states are hurting too because much of their budget is based on sales tax revenue. But what can you do when there are no sales? Free up credit? Further strangle our nation in a choke-hold of debt? Print more money?

Your government's solution was to bail out the slavers, not the slaves. To reward corruption and greed with billions of your children's tax dollars, ensuring that your children will also be slaves. Since passing the slaver bailout plan, the United States government has experimented with three different ways to spend it. None of that has your best interest in mind because it doesn't add a penny to your pocket; it just makes it easier for you borrow a penny from theirs.

Once again, all this money that is going to banks to erase invisible debt would have been better placed in the hands of working Americans with real debt. They sold invisible money; Americans acquired real debt. The slavers got caught with their hands in the cookie jar.

We are running out of both time and choices. If you subtract the illegal immigrants and the population of Americans under the age of 18, then remove all non-working and un-taxable Americans, you'd be left with well under 200 million people. Divide out that 700 billion dollars (which by the way is ours) and you'd have a stimulus package totaling around $13,000 for my family of two working adults. That's a bailout ladies and gentlemen!

$13,000 of additional income to liquidate debt, to pump into the economy, to boost the Tennessee sales tax revenue, to invest in the markets.... the possibilities are endless. The government could have put requirements on the money-- forcing all working Americans with debt to put their full stimulus package toward their debt. And non-working Americans and illegals? Well they should have never been given credit to begin with. Let the slavers suffer. This action would have created liquidity-- and given real capital for the slavers who were responsible in their lending as their working slaves climbed out from under their clutches toward financial freedom.

Instead they chose to keep us slaves. And the ones that hurt the most? Working Americans. It's time for action, people. Are GM and Ford going to fail whether we bail them out or not because they have demonstrated the failure to make wise choices. We don't have to go softly into that goodnight. Write your congressman. Tell them they've rewarded quite enough stupidity, ignorance, and greed for this lifetime, and the next.

Thursday, October 30, 2008

I know I'm not stupid, but I need some help figuring this out...

So Exxon Mobile made a record 14.5 billion dollar profit in the 3rd quarter. So if that's pre-tax profit, they pay .43 cents on every dollar they make in taxes which is verifiably insane. That's a little over 6 billion dollars in total taxes they paid on that record profit, more if they paid taxes first then reported their after-tax profit. Joe Biden came out today and said he wanted to cut the 4 billion dollars in tax relief that these companies get. Somebody needs to explain the logic in this to me, because I still don't get it. If you cut out 4 billion in tax relief, then you reduce the amount you can tax at .43 cents on the dollar. Let's say it hit this quarter (I can only guess Biden means an extra 1 billion per quarter). You would lower their profits to 13.5 billion, and only take in 5.8 billion in taxes on their profit. So, your net gain is only about 500 million. Therefore you've just taken 1 billion away from the economy via its investors so that you could put 500 million back into the economy using taxes. How does this make sense?

Tuesday, October 7, 2008

What They Left Us...

I will be 39 years old this month. I'm right on the cusp of Generation X (b. between 1964 - 1981) and squarely a product of the Baby Boomer generation before me. In the late 1980's TIME magazine described us this way:

By and large, the 18-to-29 group scornfully rejects the habits and values of the baby boomers, viewing that group as self-centered, fickle and impractical.

I wouldn't quite go that far, but I would say that what the Boomers have left is a pretty stunning example to us (a few left-over drug addicts aside) of what not to become. As the Boomers now near or enter into retirement, I wonder how exactly they see their legacy?

First, the positives. Boomers demonstrated to us the value of questioning authority. Quis custodiet ipsos custodes? Government isn't always on the side of the people and while generations before the Boomers probably knew this to be true, they never had the stones to massively organize protests on college campuses, in town halls, or in mass groups walking hand-in-hand along the main streets of the United States. Boomers taught us that the "old time religion" our grandparents kept preaching was laced in hypocrisy, racism, and the fear of healthy change. All of us Gen X'ers owe our inquisitive spirit and pursuit of truth despite consequences to the Boomers.

Even so, in the process the Boomers managed to toss out the baby with the bathwater. In the scud of their empty tub where the stains of broken marriages, unwanted pregnancies, drug addition, and eventually corporate corruption and greed. In tossing out authority altogether, they tossed out every reason to be moral. They devalued the most fundamental stabilizing forces of any society with a "Don't Tread on Me" individualism.

Of course not all of them did this. Some of them went to the polar opposite and began insisting on inapplicable moral absolutism's and overtly harmful (and hypocritical) theological doctrines. They substituted Vietnam for a culture war of their own making, while we the children in Generation X were forced to watch the ensuing blood bath. Politics divided. Churches split. Heroes fell. It's been a war, not to end all wars, but rather to endure for generations. They inscribed lines not in the shifting sand, but in the irremovable fabric of our social, political, and religious landscape.

Busy fighting each other, government and merchants banded together to rob them blind. The great celebration of giving us the first two back-to-back elected Boomer Presidents, Bill Clinton and George Bush, epitomized the frail nature of this conflict. With these appointments they successfully offered America four terms of "new leadership" by way of a pervert and a moron respectively. Sadly, I voted for both of them at least once. Their offerings to the House and Senate haven't done much better, nor have their offerings to the American pulpit.

The political and religious authorities they spent their lives questioning and rebeling against were replaced by the most corrupt authorities in American history-- maybe in all American history combined.

I know there are exceptions, and thankfully I happen to serve under one. But by and large, what the Boomers left us was a legacy of what not to become. I suppose in that, we at least owe them our thanks.

Now that the economy is lurching backward from the compounded lack of wisdom and greed, it seems like they might at least get a little taste of the mess they've left Generation X to clean up before they "shake their white locks at the runaway sun." That little taste of what we will be required to clean up is what Gen X'ers call "just desserts." I just hope there are enough of us out from under the hypnotic power of Microsoft's "X-Box" to act.

By and large, the 18-to-29 group scornfully rejects the habits and values of the baby boomers, viewing that group as self-centered, fickle and impractical.

I wouldn't quite go that far, but I would say that what the Boomers have left is a pretty stunning example to us (a few left-over drug addicts aside) of what not to become. As the Boomers now near or enter into retirement, I wonder how exactly they see their legacy?

First, the positives. Boomers demonstrated to us the value of questioning authority. Quis custodiet ipsos custodes? Government isn't always on the side of the people and while generations before the Boomers probably knew this to be true, they never had the stones to massively organize protests on college campuses, in town halls, or in mass groups walking hand-in-hand along the main streets of the United States. Boomers taught us that the "old time religion" our grandparents kept preaching was laced in hypocrisy, racism, and the fear of healthy change. All of us Gen X'ers owe our inquisitive spirit and pursuit of truth despite consequences to the Boomers.

Even so, in the process the Boomers managed to toss out the baby with the bathwater. In the scud of their empty tub where the stains of broken marriages, unwanted pregnancies, drug addition, and eventually corporate corruption and greed. In tossing out authority altogether, they tossed out every reason to be moral. They devalued the most fundamental stabilizing forces of any society with a "Don't Tread on Me" individualism.

Of course not all of them did this. Some of them went to the polar opposite and began insisting on inapplicable moral absolutism's and overtly harmful (and hypocritical) theological doctrines. They substituted Vietnam for a culture war of their own making, while we the children in Generation X were forced to watch the ensuing blood bath. Politics divided. Churches split. Heroes fell. It's been a war, not to end all wars, but rather to endure for generations. They inscribed lines not in the shifting sand, but in the irremovable fabric of our social, political, and religious landscape.

Busy fighting each other, government and merchants banded together to rob them blind. The great celebration of giving us the first two back-to-back elected Boomer Presidents, Bill Clinton and George Bush, epitomized the frail nature of this conflict. With these appointments they successfully offered America four terms of "new leadership" by way of a pervert and a moron respectively. Sadly, I voted for both of them at least once. Their offerings to the House and Senate haven't done much better, nor have their offerings to the American pulpit.

The political and religious authorities they spent their lives questioning and rebeling against were replaced by the most corrupt authorities in American history-- maybe in all American history combined.

I know there are exceptions, and thankfully I happen to serve under one. But by and large, what the Boomers left us was a legacy of what not to become. I suppose in that, we at least owe them our thanks.

Now that the economy is lurching backward from the compounded lack of wisdom and greed, it seems like they might at least get a little taste of the mess they've left Generation X to clean up before they "shake their white locks at the runaway sun." That little taste of what we will be required to clean up is what Gen X'ers call "just desserts." I just hope there are enough of us out from under the hypnotic power of Microsoft's "X-Box" to act.

Monday, October 6, 2008

A possible solution?

We know that the $700 billion dollar bailout is going to fail because it does not address the fundamental issue affecting our economy: Debt. Debt affects borrowers and lenders alike and our country has been operating on debt for far too long. Credit has been too easy to obtain, not only for the working poor with bad credit, but also for our government which borrows an incessant amount of money to stay afloat.

One of the primary reasons that liquidity is missing in the market is the absence of capital, both for average middle class Americans and banks. The United States economy is ill-advised to continue leveraging itself and its populace with credit. The economy is sending us this message with every failing bank. I read this weekend that California and other states are now asking to further suckle under the teat of Federal credit. By making debt easier to obtain, expect things to get worse not better. We need new habits.

Absent from any talk about the economic crisis seems to be the daunting reality that Americans have no savings injected into the markets. Cumulative savings for Americans are in the red, meaning that 43% of them spend more money than they make every year. This is again due to the relative ease in obtaining credit. Banks are failing because Americans lean on credit and the bailout plan just made it all the easier to continue operating with a fundamentally flawed economic philosophy. In short, a ‘credit crunch’ is a symptom of a wound that we can ill afford to hide from. That wound is credit itself. Thankfully, our family has been able to avoid high interest credit card slavery and excessive debt, but many haven’t.

If wealth trickles down (and I believe it does), we can assume that debt trickles up. The grinding halt that our banks are experiencing are the products of ordinary Americans with a massive amount of capital tied up in credit.

I am a firm believer in the free market, but since it is apparent that the House and the Senate are not willing to allow the free market to run its course and thereby institute change, we have to err against our free market philosophies at least for a time. That’s what the bailout plan did and you’ll see that what I’m suggesting does as well.

Since the primary problem in our nation’s economy is debt, any solution we offer has to address this snare of credit. Our system milks us by habitually offering tax deductions for interest paid on debts. Many from the generation before me have spent the better part of 30 years floating home mortgages in exchange for lower taxes. Average Americans with whom I speak say similar things. They refuse to get out of debt because they falsely believe that by staying deep inside debt, they get tax relief. This poisonous thinking and it began it the tax code itself. Government is not doing itself or its people any favors by encouraging a culture of debt. At some point, in the long term these tax deductions must be eliminated to foster a culture of debt reduction.

In the short term, we have to “unfreeze” middle class capital (not corporation capital), thereby giving liquidity to the markets. That was the basis of the stimulus package passed by President Bush this year. It was flawed because it was a ‘no strings attached’ tax refund. I understand the philosophy: by flooding us with capital (Chinese money even, which makes me very angry) you potentially stimulate spending, raise the markets, and create jobs. It failed because it only addressed half the problem. It left debt alone.

The middle class is covered over in debt and most of them are so trapped by high interest rates on their credit cards and car payments that they will never come out from under it without assistance. Bank profits depend on this slavery to pay out investors who back the credit. You end up with a predatory system run by anti-patriots.

I would ask that the government consider temporarily requiring lenders to offer a flat, fixed interest rate on loans and remove competition from the banking markets for a temporary time on existing loans. Consider it a T-Bill for the middle class with a pre-determined due date, but this bond doesn’t add credit or imaginary capital to indebted markets, instead it reduces debt. We can call it an “I-Bill” for simplicity.

The “I-Bill” reduces the bank interest rate to something both manageable and meager for all Americans, but it has a series of strings attached to it (unlike the stimulus package). This I-Bill would have to temporarily allow consolidation for credit card and auto loan debts. I know it is contrary to the free market ideology to prevent banks from maxing profit via an unreasonable interest rate, but so is leveraging these banks with my taxes.

Suppose a home owner with a $100,000 mortgage at 6.9% and two credit cards maxed at 18% interest were allowed a free, one time refinance opportunity to consolidate debt into an I-Bill rate offered by their banks (just for the sake of example at 5%). This would free hundreds of dollars in middle class monthly budgets which are now frozen up in credit.

For the sake of example, suppose an average middle class family savings under an I-Bill refinance plan saved $200 in monthly payments. Create pre-conditions on the new, consolidated loan requiring participants to do something like the following with their monthly savings:

Choice A – apply 100% to Principle pay-down. Total projected savings after refinance must go toward paying down, or snow-balling credit card or mortgage debt. Credit card corporations like CitiBank or Wachovia get in an instant surge of additional “real” capital, not “interest” capital.

Choice B – apply 75% to Savings and Investment. Many mortgage companies (like Wells Fargo) offer investment opportunities to their clients. Participants must enter into an agreement to roll at least 75% of their savings after refinancing to an I-Bill over into a mutual fund, money market, bonds, or CD’s then leave that money untouched for the life of the loan. This again gives markets capital and nurtures financial freedom for the middle class. The remaining portion of the monthly savings is injected straight into the economy as a stimulus package all its own.

Choice C -- apply 50% to Charitable Giving. Upon procuring the refinance, participants must select a charitable organization which they plan to support with at least half their monthly savings. Of the three choices this would be the hardest to manage in terms of whether people followed through. But it would inject a massive amount of capital into the markets, and put at least half of that in the hands of churches, shelters, food pantries, and other helping agencies who are caring for the lowest economic tier in our country.

The benefits here seem almost too obvious. Imagine millions of Americans required by conditions of a low-interest loan to pump an extra $1000 per year into reducing their principle or into a savings account, or a charity. Banks get flooded with real equity, not credit capital. Americans save for the future. And all you did was require banks to consolidate debt at a lower interest rate with pre-conditions on how the extra money saved is to be used.

Your grandfather and mine knew and practiced three simple truths about money.

Don’t borrow unless you have to and when you do borrow, pay it off quick.

Save and invest your money at every opportunity to build wealth.

Give what you can to those less fortunate.

We are caught in a culture that has drifted away from the simple but effective truths of our grandparents. If the American people are unwilling to develop these habits and if the Federal Government is going to continue to bailout people who blatantly ignore them then we need a plan to develop these habits for ordinary Americans by rewarding good behavior.

Short-term consequences for I-Bill debt consolidation fall on bank share-holders who depend on the profitability of milking America through high interest loans. These men and women are no patriots. Thomas Jefferson warned us that “merchants have no country.” If their allegiance were truly to our country, they’d support a plan which infuses America with the capital (not the credit) it needs. They’d advocate for the habits of saving and giving that we need to survive the next 100 years economically. Even if we overturn the I-Bill opportunity when the markets calm down after being flooded with the real capital and liquidity from investing and principle pay down, we’ve still developed good habits rather than giving our bad habit of credit-dependence fresh legs on which to run.

Remember, any losses incurred are losses in interest, not necessarily lost equity, which is what we are seeing now. To offset investor losses, by all means use the $700 billion. It’s not real money anyway. It is credit and more credit is only further strangling our country.

Sunday, October 5, 2008

Why the "bailout" is likely to fail...

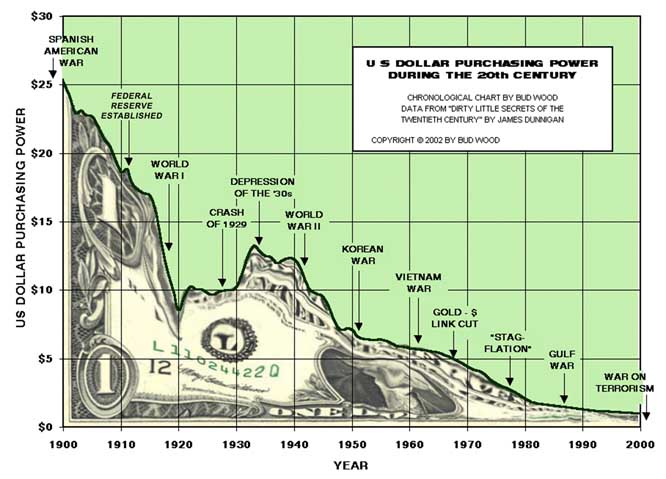

The recent 700 billion dollar bailout, coupled now with a plethora of earmarks, still fails to address the fundamental problem with our economy. That fundamental problem isn't corportation greed, although greed certainly is a problem.

The problem is pretty solidly revealed in the attached chart. It's credit. For all the talk of a "credit crunch" and the "freezing up" of credit, it doesn't appear that too many people are concerned that we already lend four times more money than we deposit.

You can see that American lending is pretty much off the chart when compared to other countries. Americans are living on borrowed money and because of that, our government is too. Maybe a freeze on credit was exactly what the doctor ordered. Making credit easier to obtain only prolongs the misery. It's like giving a drug addict an advance on his drug.

When the Feds lowered the interest rate to a remarkable level, we the people decided it was better to float our debt than to pay it off. President Bush's answer to a struggling economy was "take a vacation." The economic stimulus package he passed was an attempt to get Americans out there spending more money, buying things we don't need to impress people we don't even like.

A genuine stimulus package would have been one that reduced American debt, curbed spending at all levels, and encouraged personal savings. It's obvious when looking at the chart that America has a vastly different economic philosophy than the rest of the world. That philosophy is going to bankrupt us, because debt trickles up just as easily as it trickles down.

I've spent three weeks thinking about it, like most Americans. I've spent enough time I think to agree with most Americans that we just gone through the worst four years of Federal leadership in the history of our country. I can complain about that until I'm blue in the face. But unless I can offer another alternative, I'm part of the problem and not the solution.

Here goes.

First, allow the natural consequences to show themselves. Second, apply mercy to those consequences. If you apply mercy before you even know there is a consequence, you're not bailing anything out. You're reinforcing bad behavior. We wouldn't do that with our own children, so why would run government that way? Granted, if the situation was a dire as the pundits make it sound, we had to do something.

First, put all debt, national and personal mortgage into a level playing field with regard to interest rates. Make that interest rate be set at something insanely reasonable, but keep it at least a half point higher than the rate at which we have borrowed from the reserve (or from China). Apply the rate to mortgages, credit cards, and all forms of debt.

Under a nationwide refinance policy, instiute by law that all Americans who now have money at a lower rate and are thereby paying lower monthlies on all their debt must do one of three things with at least 75% of that money saved.

1. Save/Invest. If the lower payment on a Wachovia loan refinanced at a lower interest rate, nets a consumer an extra $100 per month, then a minimum of 75% of that money saved must be placed in a Wachovia trust fund and remain untouched for the life of the loan. The consumer receives standard interest on money saved, minus 1% which goes to Wachovia for profit.

Advantage: Benefits both the consumer and the lender. Establishes wealth and enables a mandatory retirement savings, mildly enhances consumer spending.

2. Reduction in Principle. If the lower payment on a Wells Fargo mortgage refinanced to a lower interest rate, nets a consumer an extra $200 / month in savings, then a minimum of 50% of that saved money must be applied back toward the loan's outstanding principle.

Advantage: Benefits the consumer, builds American equity, encourages home ownership, signficantly enchances consumer spending.

3. Giving. If a Citibank Visa card reduces interest rates which nets a person in debt an extra $50 per month, then a minimum of 50% of the money saved must appear on an annual charitable giving form at the end of the year.

Advantage: Benefits the consumer, encourages charitable giving, enhances consumer spending.

So any of these three habits can be used by consumers: saving/investing, principle payoff, and giving. You done nothing with real money, except potential short-changed investors in banking companies. That short-change will be short lived. To offset, use the $700 billion dollars to gradually accomdate for money lost by banks from being required to lend money at a lower rate. Do this for five years: $300 billion in year one, $200 billion in year two, $100 billion in year three, and $50 billion in years four and five.

Punishment for failing to save/invest, pay down principle, or give is also staged in increments. In year one, add 1 percentage point to every loan that does not follow the law. Year two, add 2 percentage points. Year three, add 3 percentage points. Should foreclosure ensue at any time in the three years, by the third year there should be enough capital freed up in the market to garner a really good deal on defaulted properties (from consumer spending and giving), or there will be enough real capital in the banks (from saving and investing, and principle paydown requirements) so as not to overtly effect the markets.

At the end of five years, eliminate tax reduction for interest paid. With a lower rate in the table already, the amount of pain most Americans will feel will be lessened. The government in turn gets well over $200 billion in additional tax revenue. Americans will stop floating debt to avoid taxation and that will encourage quicker reductions in debt principle. With the additional revenue the governement has from eliminating the tax deduction on interest, it can begin eliminating its own debt, while encouraging Americans to do the same.

Monday, September 22, 2008

Let the Record Show...

So a recent poll reported on CNN suggests that Americans 2/1 believe the current banking crisis is the fault of Republicans. What most Americans don't do is actually research the historical record. I must admit, when I look at eight years of the Bush Adminstration, I don't see that he personally took very much issue with the lending practices of these greedy corporations. Had I receieved a telephone survey, I probably would have laid blame on both parties.

But the record doesn't lean that way. Not at all. In fact, one candidate actually co-signed a bill for regulatory reform in our lending companies. That candidate? John McCain. The creator and additional cosigners? All Republicans. The bill, and three others just like it? Killed on the floor of the Senate, led by Democrats. Democrats who actually were taking kick-backs for their re-elections.

Here's an excerpt from an address given by John McCain on the Senate floor. Read it. Read it. Read it. Read it. Read it. Read it. Read it. Read it and learn something.

But the record doesn't lean that way. Not at all. In fact, one candidate actually co-signed a bill for regulatory reform in our lending companies. That candidate? John McCain. The creator and additional cosigners? All Republicans. The bill, and three others just like it? Killed on the floor of the Senate, led by Democrats. Democrats who actually were taking kick-backs for their re-elections.

Here's an excerpt from an address given by John McCain on the Senate floor. Read it. Read it. Read it. Read it. Read it. Read it. Read it. Read it and learn something.

The United States Senate

May 25, 2006

May 25, 2006

Section 16

Mr. President, this week Fannie Mae's regulator reported that the company's quarterly reports of profit growth over the past few years were "illusions deliberately and systematically created" by the company's senior management, which resulted in a $10.6 billion accounting scandal.

The Office of Federal Housing Enterprise Oversight's report goes on to say that Fannie Mae employees deliberately and intentionally manipulated financial reports to hit earnings targets in order to trigger bonuses for senior executives. In the case of Franklin Raines, Fannie Mae's former chief executive officer, OFHEO's report shows that over half of Mr. Raines' compensation for the 6 years through 2003 was directly tied to meeting earnings targets. The report of financial misconduct at Fannie Mae echoes the deeply troubling $5 billion profit restatement at Freddie Mac.

The OFHEO report also states that Fannie Mae used its political power to lobby Congress in an effort to interfere with the regulator's examination of the company's accounting problems. This report comes some weeks after Freddie Mac paid a record $3.8 million fine in a settlement with the Federal Election Commission and restated lobbying disclosure reports from 2004 to 2005. These are entities that have demonstrated over and over again that they are deeply in need of reform.

For years I have been concerned about the regulatory structure that governs Fannie Mae and Freddie Mac--known as Government-sponsored entities or GSEs--and the sheer magnitude of these companies and the role they play in the housing market. OFHEO's report this week does nothing to ease these concerns. In fact, the report does quite the contrary. OFHEO's report solidifies my view that the GSEs need to be reformed without delay.

Friends, I'm not asking you to vote for John McCain. For the record, I might not even be voting for him myself. I'll decide after the debates. But in the meantime, at least become an informed voter. Here's information on the other bills led by Republican Chuck Hagel, NE:

GovTrack.us. H.R. 1461--109th Congress (2005): Federal Housing Finance Reform Act of 2005, GovTrack.us (database of federal legislation) (accessed Sep 22, 2008)

GovTrack.us. S. 190--109th Congress (2005): Federal Housing Enterprise Regulatory Reform Act of 2005, GovTrack.us (database of federal legislation)

GovTrack.us. S. 1100--110th Congress (2007): Federal Housing Enterprise Regulatory Reform Act of 2007, GovTrack.us (database of federal legislation)

Too in Debt to Care as American Freedom Falls?

Welcome to your first days of socialism, ladies and gentlemen. The move by the Feds to transfer our national wealth under simple strokes of their pens is the beginning of the end. The sad thing is, most Americans are too in debt to care.

The $700 billion dollar proposed bailout marks the biggest redistribution of wealth this country has ever seen. The sad thing is that when it's all said and done, your money and mine becomes all the more imaginary. With the Federal Government in charge of brand new banking budget that doubles the Pentagon's annual budget, they can write as many checks as they want to just about whomever they want. Like sickly cows walking under the teat of American innovation and progress, the Federal Government now owns your money and mine.

The latest bailout proposal is massive and not just in dollars. It's massive in what freedoms we give up. It defaults responsibility and rewards greed. Expect things to get bigger and uglier, all this from an adminstration that promised "smaller government." Defaulted properties will quickly become property of the Feds. Do you understand that? This move puts the government over a massive number of private properties across the nation. One of the fundamental doctrines of the Constitution has been overturned by the stroke of pen. The idea of America, the idea that if you work hard you can own something for yourself and for your family, the idea that we are fighting for across the oceans, is the very idea that has crumbled on our own shores.

The enemy of capitalism at the highest levels of our nation is greed. No one, not our President and not our elected officials in Congress, took on the challenge of eliminating greed through regulation seriously-- until it was too late (amend that statement with the above blog). At the same time all this was happening, the enemy of capitalism at the grassroot level (stupidity and insecurity) ripped us apart from the inside out. We're too busy acquiring more and more and more "stuff" to successfully manage our own freedom. 43% of Americans spend more than they make every year. Is it any wonder we have a banking crisis? Hello? Anyone out there?

Perhaps the most telling thing is that this $700 billion dollars will be spent on banking corporations, not on average Americans trying to make ends meet. The bailouts average out to almost $5,000 per man, woman, and child in America. Think about it, for my family of four, that would equal somewhere between $16,000 and $20,000. Talk about a 'stimulus' package.

But what else were they going to do? The public has already demonstrated the inability to manage that kind of money. The sad thing is, the banks have already demonstrated the inability to manage that kind of money too. Now we had a third set of fingers into the American pie by allowing the Feds to manage it. Do we really expect them to do any better? Last time I checked, their debt was running in the trillions.

Game over people. We lose. Freedom loses. Our future loses. It's the beginning of the end and our forefathers are all rolling over in their graves.

Thomas Jefferson:

"Banking establishments are more dangerous than standing armies."

"Merchants have no country. The mere spot they stand on does not constitute so strong an attachment as that from which they draw their gain."

"Never spend money you haven't earned."

"Paper money will invariably operate in the body of politics as spirit liquors on the human body. They prey on the vitals and ultimately destroy them. Paper money has had the effect in your state that it will ever have, to ruin commerce, oppress the honest, and open the door to every species of fraud and injustice."

-- George Washington

"A great industrial nation is controlled by it's system of credit. Our system of credit is concentrated in the hands of a few men. We have come to be one of the worst ruled, one of the most completely controlled and dominated governments in the world--no longer a government of free opinion, no longer a government by conviction and vote of the majority, but a government by the opinion and duress of small groups of dominant men."

-- Woodrow Wilson

Tuesday, September 16, 2008

Fixing Our Financial Crisis with Common Sense...

Let's take a quick look at what's happening. Lending companies are going in the tank and that's effecting Wall Street, the housing markets, and the value of the dollar. People are quick to point fingers at Federal policy... maybe that's part of it. But the majority of the story and the blame, really belongs elsewhere. Let's look briefly at the foolish new American past time known as "Subprime Lending."

Subprime loans can be helpful, especially when coupled with a loan at prime for qualified buyers who are relatively stable in employment, and who are purchasing a home in which they plan to stay. But truthfully, even in those circumstances, they aren't a wise way to go. People end up leaving a lot to chance and can quickly get themselves into a heap of debt for which they have no income to escape from...

Even at that, there are far too few of these kinds of "rational" subprime loans being administered by these failing companies. Instead, there are many other types of "whacky" loans being granted to people who do not qualify for regular prime loans.

From wiki, some of these include loaning money to people who are in credit trouble. For example, they have issues because they have:

- Two or more loan payments paid past 30 days due in the last 12 months, or one or more loan payments paid past 90 days due the last 36 months;

- Judgment, foreclosure, repossession, or non-payment of a loan in the past;

- Bankruptcy in the last 7 years;

- Relatively high default probability as evidenced by, for example, a credit score of less than 620 (depending on the product/collateral), or other bureau or proprietary scores with an equivalent default probability likelihood.

Now I'm no genius, but here's a simple newsflash: stupid is as stupid does. What on earth do lenders think is going to happen when you loan money to people with a shaky track-record of paying back past debts? How would an increased interest rate, or an interest-only loan, lead people with demonstrated deficiencies in managing money to financial independence?

Again, I'm no genius, but here's a possible solution -- don't lend money to people who won't pay it back. Unless bankruptcy is something you desire, this probably isn't the way to do business. Is it any wonder you're short on capital when you just spent your hours roping in loans from people that can't get them anywhere else? These guys should be removed from the economic market, not bailed out by the Feds. That part, Obama has right. They should be held accountable for making stupid decisions.

And here's another tidbit of advice: Don't borrow money you won't pay back. I know we have to keep up with the Jones' and all, but come on. Pay off your debt before you go gobbling up more. Live simply and with a meager humility. Pay what you owe. Build your net worth, when you've demonstrated you can do that, maybe you're ready to borrow some big cash. Until you can be faithful in the small things -- like your credit card debt -- don't even think about jumping into the big leagues. Turn off your cell phone. Cancel your cable. Eat hotdogs and spaghetti for a year. Frame a photograph and make that your Christmas gift until you can afford those pretty pearl earrings for mom. Hello? Is anybody out there listening?

Our financial woes have very little to do with "policy." They've got everything to do with the average American Joe out living large, writing checks his account can't cash, and getting himself in a pickle. Stand-up against ignorance people. Don't buy into the hype. Take accountability for your own life and make our American history proud. My grandfather is rolling over in his grave about now.

Let me summarize it again, for any who might have missed it:

1. Don't lend money to people who won't pay it back.

2. Don't borrow money you won't pay back.

OK, are we all clear on this? If we can spend the next ten years living the way we were intended to live the last ten years, then our financial institutions will be just fine. I give you back to your regularly scheduled absurdity.

Tuesday, September 2, 2008

Vultures and Corpses...

So... I was perplexed this morning during my quiet time. I was reading from the Gospel of Luke and found something Jesus said:

"Where the corpses are, there the vultures will gather."

It seemed like a really odd thing for him to say. I read a bit of the context and the disciples were asking Him about the end times. He basically gave them a few details, but they pressed him further -- They asked, "Where is all this going to happen?"

Jesus said, "Where the corpses are, there the vultures will gather."

It is engimatic question. The references and study guides were of no help at all. They all pointed to the end times jargon that fills way too many pages of books, and consumes way to many of our best minds in meaningless speculation.

So I got a revelation in the shower -- God mostly speaks to me in the shower. If you've read this blog at all, you've heard me say this. The revelation was simple: Jesus was basically insulting them for even asking the question. Think about it, they're bugging him about details and he quips about gathering around dead bodies.

A modern translation would read something like this: "Hey Jesus, you say all this bad stuff is going to happen, tell us where." Jesus pondered a moment and said, "Stop rubber-necking the trainwreck."

In other words, quit being so dang consumed about who's going down, when it's going down, and where it's going to be. Do you want to be a vulture? Is death all you care about? Focus on life, cause that's what I am about.

You ever meet those kind of people that seem to only want to give you the bad news? I mean as soon as you walk in the door, they are full of information about who has cancer, who just died, whose wife just left them... you know the kind, glass half-empty people feasting off everyone else's disasters.

I think it kind of grates of Jesus' nerves after a while. He'd heard enough. He spouted off... "You're like a bunch of vultures, circling around my every word looking for doom and gloom." In so many words, I think he told the disciples to shut up and get on with living.

Maybe that's what we should say when the folks around us are so concerned with the misfortune of others that they can't even live their own lives with grace and dignity. I'd like to say, that's just a thought. But it's not. It's a Word. Take it how you will.

"Where the corpses are, there the vultures will gather."

It seemed like a really odd thing for him to say. I read a bit of the context and the disciples were asking Him about the end times. He basically gave them a few details, but they pressed him further -- They asked, "Where is all this going to happen?"

Jesus said, "Where the corpses are, there the vultures will gather."

It is engimatic question. The references and study guides were of no help at all. They all pointed to the end times jargon that fills way too many pages of books, and consumes way to many of our best minds in meaningless speculation.

So I got a revelation in the shower -- God mostly speaks to me in the shower. If you've read this blog at all, you've heard me say this. The revelation was simple: Jesus was basically insulting them for even asking the question. Think about it, they're bugging him about details and he quips about gathering around dead bodies.

A modern translation would read something like this: "Hey Jesus, you say all this bad stuff is going to happen, tell us where." Jesus pondered a moment and said, "Stop rubber-necking the trainwreck."

In other words, quit being so dang consumed about who's going down, when it's going down, and where it's going to be. Do you want to be a vulture? Is death all you care about? Focus on life, cause that's what I am about.

You ever meet those kind of people that seem to only want to give you the bad news? I mean as soon as you walk in the door, they are full of information about who has cancer, who just died, whose wife just left them... you know the kind, glass half-empty people feasting off everyone else's disasters.

I think it kind of grates of Jesus' nerves after a while. He'd heard enough. He spouted off... "You're like a bunch of vultures, circling around my every word looking for doom and gloom." In so many words, I think he told the disciples to shut up and get on with living.

Maybe that's what we should say when the folks around us are so concerned with the misfortune of others that they can't even live their own lives with grace and dignity. I'd like to say, that's just a thought. But it's not. It's a Word. Take it how you will.

Friday, August 8, 2008

My vacation was rough...

Myrtle Beach... sun, sand, extreme noise. I caught a virus on the first day. Bad sore throat every night, coupled with incessant hacking, coughing, and sneezing. Our condo was right on the strip. Cars, motorcycles, bass cranked so loud it rattled the windows in our room until 3:00 AM every night. Gah. This was supposed to be relaxing!

On the plus side, I got some great time with the fam. And I wrote like a mad-man. I think I finished over 20 pages of script and a synopsis or two. :)

Sunday, June 15, 2008

If you take a world champion to a comic convention....

So I've spent a few years now reading the "If you take a mouse to the movies..." stories to my kids. What happens if you take a world championship Brazillian to a comic convention?

If you take a world champ to a comic convention,

he might ask to dig through all the Spawn action figure boxes...He'll buy some, then lay them down at the Star Wars boxes...

If you offer to carry them, he'll let you.

Then he'll start hunting down Wolverine items...

and grub.

He'll frown on your high carb plate, and caffine beverage.

And laugh when you tell him it's a special training diet.

Then, he'll visit the artists...

and they'll love him,

even though the conversation tends to steer away from cubism or dadism.

If you take a world champ to a comic convention,

he'll get cool perks, and maybe even some free stuff.

He'll make new friends, and you will too.

He'll hold your Green Arrow stuff for you,

while you rummage the boxes for back issues you missed.

You'll debate how much you want to spend,

and on what.

He'll tell the comic artists and writers

how much you talk about them,

everyday before training.

If you take a world champ to a comic convention,

you're both going to have some fun...bond a little bit off the mats...

Share a new technique...

...one that doesn't leave a bruise.

:)

As of Sunday, June 8 -- Samuel Braga is a six time Brazillian Jujitsu champion. He's visiting a little town in East Tennessee, making new friends, helping us build a school of quality trainers... he may be here a while, who knows?

Samuel is probably the most humble person I've ever met in my entire life. To have accomplished so much, and to be at the top of his game, yet still as down to earth as anyone you'll ever meet is a testament to the Gracie Barra school, Samuel's parents who raised him well, and Samuel himself -- who is a good Christian man.

He reminds me how far I have to go in my journey -- not only as a fighter, but as a human being.

And yeah, he LOVES comics.

We met some fantastic people, who lifted some of my own cynical attitudes about the industry. They humbled me just as Samuel did -- professionals at the top of their game.

What a great day!

Saturday, February 2, 2008

The Robe

So I can look a little stodgy in the robe, I realize this. It’s really not my style at all, so when I put it on there is usually a good reason. I pretty much will only wear the robe to “marry or bury” as they say, but even then I won’t wear it unless I’m asked. There’s just something superficial about looking “the part” and I’ve rejected appearances the entire seventeen years I have been a minister.

As if my long hair and goatee during this time of my life weren’t enough, I decided the least I could do is preach in jeans and a ball cap every Sunday. I wasn’t really trying to throw anyone curve balls; more like trying to get people to stop playing the game altogether. That’s all behind me now of course. There’s an old saying that goes like this:

“If you haven’t bucked the system before you turn thirty, then you’ve got no heart; and if you haven’t joined it after thirty, then you’ve got no brains.”

Needless to say, when they stand over me in the funeral parlor, it’s going to be those “heart” years that make them laugh, while at the same time make the dead man blush beneath the mortician’s paint. It won’t be quite the same as “rolling over in the grave,” but certainly akin.

Given such, I supposed long ago it would be better to let the embarrassment loose before I shake off this mortal coil and thus I currently manage to weave a complex honesty into my messages each Sunday. This sort of honest sharing is a mixed blessing and probably runs off as many congregants as it attracts. Last time I checked, the same was true of Jesus. I try not to beat myself up over it.

Being the first of these little tales I’ve put to ink, I beg your apologies for you will soon discover that I do tend to ramble and chase bunnies at times. I started this yarn with that pompous old black robe. Although I shouldn’t frown on it since it was gift given to me at my ordination, a gift that has probably saved me hundreds of dollars over the long haul.

Anyway, I was asked to do a wedding. This happens a great deal to ministers and believe it or not, a minister will get about ten times as many calls from people outside his congregation for weddings and funerals than his own church-goers. It’s the “outside” events that sometimes make pastors nervous. Some preachers won’t even consider doing a wedding for a couple that doesn’t go to their church, but something about that policy never sat well with me. I tend to hear people out.

In this particular circumstance, the couple already had a pastor committed to do the service, but during pre-marital counseling it was revealed that the groom was Jewish. He wasn’t just Jewish; he was committed to staying Jewish. In spite of having known the bride all her life, this Christian pastor elected not to do her wedding. The problem was real simple: the wedding day was only two short weeks away when the proverbial cat got let out of the bag; therefore, besides “being unequally yoked” as the good book puts it, they were in all likelihood not going to have anyone but the county judge willing to yoke them at all.

The young man’s rabbi was equally distraught and torn at his selection of a Christian bride. Nevertheless, after much convincing, the couple managed to talk the old man into doing a ceremony. Even so, the bride was still very disappointed at the thought of not having a Christian wedding. I’ve always been a sucker for people in desperate situations. Through the tears and multiple objections, I finally agreed to help. This young lady’s desire to make Jesus a part of her ceremony was touching, but was probably going to stir a great big hornet’s nest with the groom’s family, and his rabbi.

I met with the rabbi later that week. It was a cordial meeting: I in my long hair and goatee, and he in all his wrinkled glory. The man had to be every bit of 80 years old. We worked together on how to best handle our religious differences and how to structure a ceremony that we both had reservations about doing. Of special importance to this story, I agreed to wear that dastardly robe.

I should have insisted on no robe because this was to be an outdoor wedding. It was June and June days in Tennessee can go one of three directions: perfect, raining, or a post-rain sweltering kind of heat. As it happened, the day began with rain. I glanced out the window of my apartment and fretted to myself. It was going to be one of those days.

Jumping in the shower, I had my morning prayer. I always pray in the shower. It’s quiet, private, and relaxing. There’s this old church hymn we sing that says, “As we gather may your Spirit work within us…” Ever since I was kid, I’ve been singing that song, “As we lather...” It’s only natural that I find God as I lather in Ivory soap and that incredible .98 cent White Rain shampoo (I recommend the “passion flower” scent for a more heavenly experience).

During my prayers, I asked God to help me connect with an audience that would be at least half Jewish. I had already selected some passages from Ruth, and 1st Corinthians 13 in the New Testament. I had a rabbi friend tell me once that 1st Corinthians 13 was the essence of all true religion, so I felt safe with that.

I jumped out of the shower thinking to myself once again that I was going to have to grow up and get a hair cut some day. I dried off and paraded my naked flesh over to the underwear drawer. I faced the usual dilemma, would it be boxers or briefs? Since I was going to have to wear the robe, and I hated wearing the robe, I selected a bright green pair of Marvin the Martian boxers to wear. I would at least have a minor rebellion in my attire.

I’ve always loved cartoons and Marvin the Martian was probably at the top of a really short list of characters for me personally. When I was in high school, I used to run around saying “Oooohhh, you are making me very ANGRY,” while using my best Martian voice. (I know I was a geek in high school.) Black pants, white shirt, conservative tie finish the wardrobe and I’m out the door, with the robe folded over in my hands.

I arrive at the wedding site and rain is starting to taper off slightly. Friends of the bride and groom milled about under umbrellas as the clouds slowly dissipated. Within an hour, the sun was beating down on us unencumbered by clouds. That steamy feeling started to overtake me, and it wasn’t the same one I got from one of the bridesmaids after telling her I was single. This was a miserable kind of steam, the sauna variety.

Folks were taking their places and it was time for me to don the robe. The wedding was being held at a country club estate, with a nice multi-seated bathroom just across from the gazebo under which the couple would exchange vows. I quickly headed inside the restroom to put on the robe. All fifteen pounds of it slid over my head and fell down to my ankles. I immediately began to sweat. I grabbed some paper towels and dabbed my forehead, then exited and made my way to the groom.

He was nervous. They always are in my experience. A few pats on the back, a comforting word, or a quick prayer seem to do the trick. Our music cued up, and we walked out to the front of the gazebo. It was a huge audience. I never get nervous when I preach, but because I’m a blue jeans kind of preacher, I’ve always been a bit apprehensive at weddings, usually even more nervous than the groom I’m trying to comfort. Of course, no one ever pats my back, or offers me a comforting word—at least not until all is said and done. It is the thankless life of minister, one in which you are graded by performance alone, showmanship as it were—the very thing I'm not good at.

Needless to say, the sweat began to pour out of me even more. The next song began and in filed the bridesmaids. The one I was talking with earlier sort of gave me a look. Yikes! I had to stay focused. Then right on schedule, the bride marched her way down the center of the lawn, which still glistened from the morning rain. It was truly beautiful, and it always is beautiful to see a new bride. Of course, I would have to say that bit about the rain glistening out loud, and then mention sun coming out just before we started, and the glory of sunshine, and then a bit about flowers; all that stuff preachers say right before they go medieval on you in a wedding. So, I said it all (afterall, I was wearing 'the robe.')

I opened up the Bible to the passages I selected earlier that week. The sun was beating down on me, and I mean beating down hard. Sweat began dripping off my forehead onto the page, onto my notes. It was such a salty sweat that some of it began dripping into my eyes and they began to sting. Spat, splat. The book of Ruth never had this much rhythm, even with the sweet lover curled up at the feet of Boaz. Each bead of sweat literally bounced off the text.

By the time I got to 1st Corinthians, I had a much different problem: something was crawling up my sock. I blamed the robe. It was wide and offered the little critter the cover of darkness through which to explore the incredible world of my ankle. I kept on reading as though nothing was happening.

“Love is patient, love is kind…”

Whatever creature had taken interest in me got really brave. It set a course up my leg like Christopher Columbus on steroids. Around the knee, I started to get very worried. I thought about the boxers for a second and the sweat cut loose like rain. I began to fidget as I finished the passage from St. Paul. I glanced up from the text and looked at the crowd. They had no idea I was struggling. My gaze turned to the rabbi beside me. He looked like he’d just seen Elvis crossing the yard. We exchanged a single glance and he knew I was in real trouble.

After the scripture, I politely yielded to the gentle old man and he gracefully took over. By this time, I knew that the creature in my pants leg was an insect. The bug had worked its way to my thighs. Not wanting to make a scene, I reached down to place my hands in the pockets to brush the creature back down my leg. To my dismay, I didn’t have any pockets. I was wearing the robe.

I shook my leg as unobtrusively as possible under the robe. This caused the insect to become fearful and work doubly hard to arrive at whatever destination it had determined. The boxers made for easy access.

The rabbi was breaking out the glass for the couple to stomp. I knew this had to be near the end. As he began to speak, my new found friend settled in a quiet fold beneath the scrotum. I committed myself that no matter what happened, I would not reach down and touch, scratch, or rearrange my privates in front of all these people.

“Mazal Tov!” The shout from the crowd and the shifting of the bride and groom on the stage caused me to have to move slightly left of center. The identity of my testicular guest became clearer with a sharp sting. Zap! My buttocks shot backward and up at a forty-five degree angle. With the music now going and people clapping and singing, I think my hop may have actually seemed somewhat normal. The tears must have seemed normal too because no one was affected by my instantaneous weeping… wait, no. One person was affected. My dear fellow clergyman, the rabbi—he just kept staring at me with those dark, beady eyes. He still knew something was wrong with the hippie Christian pastor. I’m not sure what he knew, but what I knew was that I had the pressing urge to grab my crotch. Honestly, that’s all I needed.

Immediately after the couple’s family had been escorted out, I invited the crowd to stay for the reception that had been planned. I dismissed us in prayer as best (and as quickly) as I could. Shaking no hands and speaking with no one I ran straight for the bathroom next to the gazebo.

The door to the bathroom flew open and I immediately reached down to grab the hem of my robe. I never considered getting in a stall, or locking the door. With one swoop, I threw the robe up over my head. Quickly I unfastened my dress pants and jerked them to the floor. I began rubbing and patting and shaking my crotch to get the bee out.

Suddenly, I heard the door to the bathroom open. I lowered my robe just enough to see who entered. It was the rabbi, his mouth shot open in amazement, eyes bulging out of his head at the sight of me: robe high, trousers low beating my private parts feverishly atop the Marvin Martian underwear.

“There was a bee in my pants.” I said.

For some reason, I knew it was too late. The damage had already been done. The old man just nodded and said, “Uh-huh.” Then he turned and walked out without another word.It really wasn't my most mortifying thing ever, but I'm fairly sure it was his.

As if my long hair and goatee during this time of my life weren’t enough, I decided the least I could do is preach in jeans and a ball cap every Sunday. I wasn’t really trying to throw anyone curve balls; more like trying to get people to stop playing the game altogether. That’s all behind me now of course. There’s an old saying that goes like this:

“If you haven’t bucked the system before you turn thirty, then you’ve got no heart; and if you haven’t joined it after thirty, then you’ve got no brains.”

Needless to say, when they stand over me in the funeral parlor, it’s going to be those “heart” years that make them laugh, while at the same time make the dead man blush beneath the mortician’s paint. It won’t be quite the same as “rolling over in the grave,” but certainly akin.

Given such, I supposed long ago it would be better to let the embarrassment loose before I shake off this mortal coil and thus I currently manage to weave a complex honesty into my messages each Sunday. This sort of honest sharing is a mixed blessing and probably runs off as many congregants as it attracts. Last time I checked, the same was true of Jesus. I try not to beat myself up over it.

Being the first of these little tales I’ve put to ink, I beg your apologies for you will soon discover that I do tend to ramble and chase bunnies at times. I started this yarn with that pompous old black robe. Although I shouldn’t frown on it since it was gift given to me at my ordination, a gift that has probably saved me hundreds of dollars over the long haul.

Anyway, I was asked to do a wedding. This happens a great deal to ministers and believe it or not, a minister will get about ten times as many calls from people outside his congregation for weddings and funerals than his own church-goers. It’s the “outside” events that sometimes make pastors nervous. Some preachers won’t even consider doing a wedding for a couple that doesn’t go to their church, but something about that policy never sat well with me. I tend to hear people out.

In this particular circumstance, the couple already had a pastor committed to do the service, but during pre-marital counseling it was revealed that the groom was Jewish. He wasn’t just Jewish; he was committed to staying Jewish. In spite of having known the bride all her life, this Christian pastor elected not to do her wedding. The problem was real simple: the wedding day was only two short weeks away when the proverbial cat got let out of the bag; therefore, besides “being unequally yoked” as the good book puts it, they were in all likelihood not going to have anyone but the county judge willing to yoke them at all.

The young man’s rabbi was equally distraught and torn at his selection of a Christian bride. Nevertheless, after much convincing, the couple managed to talk the old man into doing a ceremony. Even so, the bride was still very disappointed at the thought of not having a Christian wedding. I’ve always been a sucker for people in desperate situations. Through the tears and multiple objections, I finally agreed to help. This young lady’s desire to make Jesus a part of her ceremony was touching, but was probably going to stir a great big hornet’s nest with the groom’s family, and his rabbi.

I met with the rabbi later that week. It was a cordial meeting: I in my long hair and goatee, and he in all his wrinkled glory. The man had to be every bit of 80 years old. We worked together on how to best handle our religious differences and how to structure a ceremony that we both had reservations about doing. Of special importance to this story, I agreed to wear that dastardly robe.

I should have insisted on no robe because this was to be an outdoor wedding. It was June and June days in Tennessee can go one of three directions: perfect, raining, or a post-rain sweltering kind of heat. As it happened, the day began with rain. I glanced out the window of my apartment and fretted to myself. It was going to be one of those days.

Jumping in the shower, I had my morning prayer. I always pray in the shower. It’s quiet, private, and relaxing. There’s this old church hymn we sing that says, “As we gather may your Spirit work within us…” Ever since I was kid, I’ve been singing that song, “As we lather...” It’s only natural that I find God as I lather in Ivory soap and that incredible .98 cent White Rain shampoo (I recommend the “passion flower” scent for a more heavenly experience).

During my prayers, I asked God to help me connect with an audience that would be at least half Jewish. I had already selected some passages from Ruth, and 1st Corinthians 13 in the New Testament. I had a rabbi friend tell me once that 1st Corinthians 13 was the essence of all true religion, so I felt safe with that.

I jumped out of the shower thinking to myself once again that I was going to have to grow up and get a hair cut some day. I dried off and paraded my naked flesh over to the underwear drawer. I faced the usual dilemma, would it be boxers or briefs? Since I was going to have to wear the robe, and I hated wearing the robe, I selected a bright green pair of Marvin the Martian boxers to wear. I would at least have a minor rebellion in my attire.

I’ve always loved cartoons and Marvin the Martian was probably at the top of a really short list of characters for me personally. When I was in high school, I used to run around saying “Oooohhh, you are making me very ANGRY,” while using my best Martian voice. (I know I was a geek in high school.) Black pants, white shirt, conservative tie finish the wardrobe and I’m out the door, with the robe folded over in my hands.

I arrive at the wedding site and rain is starting to taper off slightly. Friends of the bride and groom milled about under umbrellas as the clouds slowly dissipated. Within an hour, the sun was beating down on us unencumbered by clouds. That steamy feeling started to overtake me, and it wasn’t the same one I got from one of the bridesmaids after telling her I was single. This was a miserable kind of steam, the sauna variety.

Folks were taking their places and it was time for me to don the robe. The wedding was being held at a country club estate, with a nice multi-seated bathroom just across from the gazebo under which the couple would exchange vows. I quickly headed inside the restroom to put on the robe. All fifteen pounds of it slid over my head and fell down to my ankles. I immediately began to sweat. I grabbed some paper towels and dabbed my forehead, then exited and made my way to the groom.

He was nervous. They always are in my experience. A few pats on the back, a comforting word, or a quick prayer seem to do the trick. Our music cued up, and we walked out to the front of the gazebo. It was a huge audience. I never get nervous when I preach, but because I’m a blue jeans kind of preacher, I’ve always been a bit apprehensive at weddings, usually even more nervous than the groom I’m trying to comfort. Of course, no one ever pats my back, or offers me a comforting word—at least not until all is said and done. It is the thankless life of minister, one in which you are graded by performance alone, showmanship as it were—the very thing I'm not good at.

Needless to say, the sweat began to pour out of me even more. The next song began and in filed the bridesmaids. The one I was talking with earlier sort of gave me a look. Yikes! I had to stay focused. Then right on schedule, the bride marched her way down the center of the lawn, which still glistened from the morning rain. It was truly beautiful, and it always is beautiful to see a new bride. Of course, I would have to say that bit about the rain glistening out loud, and then mention sun coming out just before we started, and the glory of sunshine, and then a bit about flowers; all that stuff preachers say right before they go medieval on you in a wedding. So, I said it all (afterall, I was wearing 'the robe.')